The claims processing lifecycle: What P&C carriers need to optimize from FNOL to settlement

According to the JD Power 2024 U.S. Claims Digital Experience Study, the average claims cycle time has climbed to 23.9 days, up more than six days since 2022. Yet, policyholders expect resolution in 11 days. That gap is where loss adjustment expense (LAE) accumulates, Net Promoter Scores (NPS) erode, and competitors with faster, digital-first experiences gain ground.

The good news: Most of the friction that drives cycle time higher is concentrated in a few predictable stages of the claims processing lifecycle. When you identify those stages and address the root cause, the improvements compound across your entire operation.

This guide breaks down claims processing from first notice of loss (FNOL) through final settlement, maps the most common sources of friction at each stage, and details the optimization strategies that leading Property & Casualty (P&C) carriers are using to close that gap.

It draws on Assured's experience supporting carriers across millions of claims interactions, where structured data at intake has proven to be the most important lever for downstream claims automation.

Assured: The leading AI platform in P&C

Trusted by the nation’s top insurers, Assured processes tens of millions of claims each year, delivering straight-through processing at enterprise scale.

Learn moreWhat is claims processing?

Claims processing is the end-to-end lifecycle of a claim, beginning with FNOL and ending with settlement and closure. It includes intake, verification, investigation, evaluation, communication, payment, and post-settlement activities such as recovery, audit, and reporting.

Effective claims management in insurance depends on a chain of handoffs between people, channels, and systems. At each step, decisions depend on what information is present, what is still needed, and how reliably that information can be validated. This is why data quality at FNOL matters so much. When your initial claim data is complete, structured, and machine-readable, every downstream step moves faster. Triage is more accurate. Investigation starts with context. Customers receive relevant follow-ups instead of redundant questions.

Assured’s approach is to ground automation in quality data from the start. By combining structured intake with embedded AI-powered solutions, Assured helps keep claims progressing through each stage with minimal friction.

Why the insurance claims process matters for P&C leaders

Understanding the full insurance claims process separates incremental improvement from systemic performance gains. You may already be optimizing individual stages, but lifecycle visibility reveals why performance varies across lines of business, jurisdictions, channels, and teams.

Three executive-level metrics tend to move together:

- Cycle time measures how quickly a claim reaches resolution or repair.

- LAE captures the cost to handle the claim, including adjuster time and vendor overhead.

- Customer experience, often measured as satisfaction rate, complaint rate, or NPS, reflects how policyholders perceive the process from start to finish.

Every stage of the insurance claims process, from FNOL through final settlement, contributes to all three.

Yet most carriers still manage that lifecycle in fragments: Siloed systems, inconsistent intake channels, manual handoffs that introduce variance at every step, and communication scattered across disconnected tools.

That fragmentation has a compounding cost. When data collected at FNOL is incomplete or unstructured, every downstream decision becomes slower and less reliable. Adjusters spend more time reconstructing what happened. Vendors wait longer for instructions. Policyholders are left without updates.

Modern policyholders have also raised the bar. They expect transparency and digital-first communication, the same experiences they receive from retail and financial services. Carriers that deliver those experiences earn loyalty and retention.

Automation changes this equation. When you build on a structured data foundation for claims, you gain the ability to reduce administrative burden on adjusters, improve routing accuracy, and create predictable outcomes across your organization. Lifecycle visibility is what makes that possible, and claims processing improvements become systemic rather than incremental.

The claims processing lifecycle: A stage-by-stage breakdown

While there is variance across lines of business and claim types, the claims processing lifecycle follows a consistent arc: FNOL, verification, investigation, evaluation, communication, settlement, and post-settlement work. The opportunities for claims automation are similarly consistent at each stage. They all rely on capturing complete, quality data early, then enabling downstream automation through intelligent AI solutions.

Stage 1: First notice of loss (FNOL)

FNOL sets the foundation for all downstream decisions. When early data is complete, structured, and standardized, triage is more accurate, investigation begins with full context and customers move through the process without redundant follow-up questions.

The fastest path to better FNOL is structured intake. Structured intake reduces back-and-forth, eliminates rekeying, and improves the eligibility of claims for straight-through processing. This is where claims automation pays off immediately.

Assured’s digital FNOL solution captures structured, machine-readable data from the first interaction, using dynamic flows with more than 1 billion permutations that adapt in real-time and enrichment from 60+ external data sources.

Stage 2: Policy verification and eligibility

Once FNOL data is captured, verification determines whether the claim falls within policy terms. When policy data is mapped to structured fields from intake, verification becomes faster, more consistent, and easier to audit. Your adjusters spend less time toggling between systems and more time advancing claims that are ready for the next step.

Stage 3: Investigation and documentation

Investigation is where complexity shows up. Statements, photos, estimates, third-party documents, and police reports arrive in different formats across different channels. Straightforward claims move faster when documentation is collected early and organized in a way that supports evaluation. Assured’s digital First Contact solution reaches out to all involved parties automatically to streamline documentation collection.

AI is particularly useful at this stage. It classifies documents, extracts relevant facts, identifies missing items, and prompts targeted follow-ups. Emma, Assured’s agentic AI assistant, autonomously collects data and documents, keeping the file progressing without tying up adjuster time.

Stage 4: Liability and exposure evaluation

Liability and exposure evaluation determine the handling path and settlement strategy. Consistent evaluation depends on complete, up-to-date information. When early data is thorough and the file is updated as new facts emerge, leakage decreases.

AI supports this stage by identifying inconsistencies and standardizing how exposure signals are surfaced. It ensures your adjusters see the right facts, in the right format, at the right moment, so their judgment is informed by the most complete picture available.

As data is collected, it becomes possible to identify fraud. Assured’s proactive Fraud solution continuously perceives, predicts, and prevents fraud in real time.

Stage 5: Communication and routing

Communication is where many claims organizations have the greatest opportunity for efficiency gains. Conversations occur across email, text, phone calls, and other channels. Vendors and internal teams need updates. Customers want visibility.

Assured’s omnichannel claims communication solution consolidates all of these exchanges into a structured thread tied to the claim. When your adjusters can see every interaction in one place, follow-ups are timely, inbound status calls decrease, and audits become straightforward.

Stage 6: Settlement and payment

Settlement depends on decision readiness. When the file is complete and verified, it’s faster and more consistent. Complete files also reduce the back-and-forth that extends cycle time. Automation supports settlement by accelerating document collection, validating submissions, and keeping both claimant and adjuster aligned on what comes next.

Stage 7: Post-settlement activities

After settlement, recovery, subrogation, fraud review, reporting, and audits all rely on clean, consistent data. A structured, machine-readable claim record is what makes post-settlement work scalable.

Structured records also enable better feedback loops. You can measure where claims progress most efficiently, which questions or documents predict faster resolution, and where your workflow delivers the strongest results.

Operational bottlenecks that slow claims processing

Now that you have seen what each stage looks like when it works well, it is worth examining where claims processing most commonly loses momentum. If your organization feels busy but claims are progressing slowly, the issue is rarely adjuster effort. The same friction points appear across carriers regardless of staffing levels or system investments, because the root cause is structural.

The most common friction points in claims processing include:

- Incomplete or unstructured FNOL data that requires follow-up and interpretation before downstream work can begin

- Manual data re-entry across systems, spreadsheets, and email threads that introduces errors and delays at every handoff

- Repeated document collection requests that stall coverage decisions and extend cycle time

- Limited real-time updates that drive inbound calls and escalations, consuming adjuster capacity

- Disconnected communication channels that leave policyholders waiting for answers and adjusters chasing context

Some carriers choose to outsource insurance claims processing for specific functions, such as document review, first-party investigations, or catastrophe overflow. Outsourcing can add temporary capacity, but it works best when paired with improvements to the underlying data.

When data arrives complete and structured, external teams can work at the same speed and consistency as internal staff. The decision to outsource insurance claims processing becomes more effective when the data foundation supports it, rather than shifting the same rework to a different team.

Where claims processing breaks: The compound effect of poor data

These bottlenecks are easier to address when you see how they connect. A typical pattern in claims management in insurance looks like this:

- Intake arrives with missing details or in a format that does not map cleanly into the core system.

- Triage becomes conservative because it lacks confidence, so more claims are routed to adjusters even when they could be handled straight through.

- Adjusters spend the first day collecting basics: photos, loss location details, vendor preferences, proof of ownership, receipts, or a clearer statement.

- Customers call for status updates because they have not received proactive communication, creating additional work at every level.

- Evaluation stalls because the file is incomplete, and settlement becomes a series of follow-ups rather than a single decision.

Each step compounds the one before it. A claim that starts with incomplete data accumulates friction at every subsequent stage.

Structured data is not a "nice to have." It is the determining factor for downstream automation.

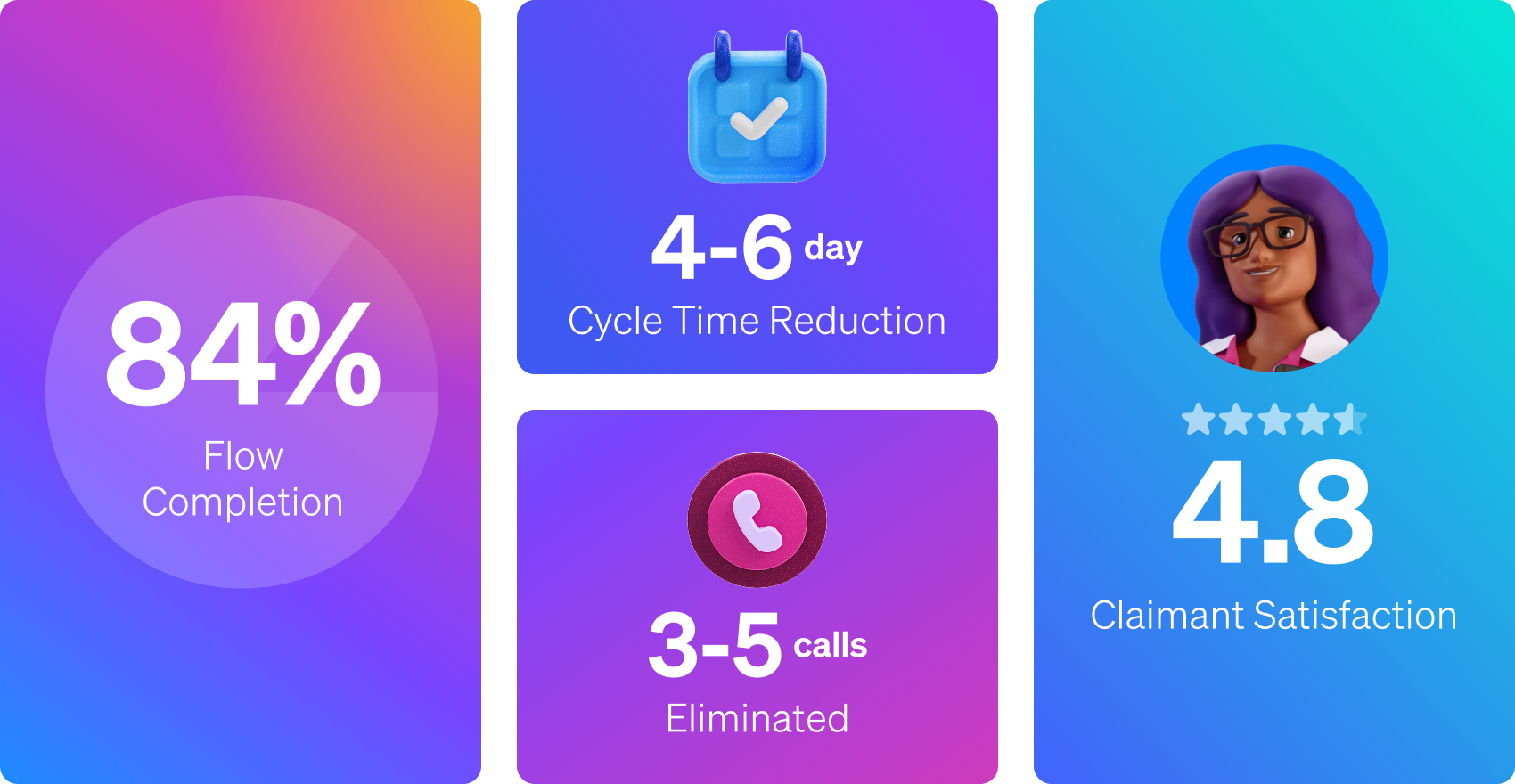

Assured has seen this pattern resolve at scale. Better intake data reduces rework, shortens cycle time by 4 to 6 days, and eliminates 3 to 5 phone calls per claim by shifting routine exchanges into structured digital workflows.

Optimization strategies for each stage of the claims processing lifecycle

Understanding the compound effect of poor data points directly to the solution: Improve data quality and workflow consistency from the very first interaction. The following strategies allow you to standardize inputs, reduce handoffs, and automate repetitive work at each stage of claims processing.

Strategy 1: Collect quality data at FNOL

- Use structured FNOL flows instead of open-ended intake to gather quality data from the start

- Enrich claims with external data to fill gaps and verify details early

- Leverage AI and business rules to optimize flows for optimal user experience and completion rate

Strategy 2: Streamline document collection

- Trigger document requests immediately after FNOL for common claim types

- Provide clear instructions to increase the rate of usable submissions

- Use AI to autonomously and proactively collect and verify incoming documents

Strategy 3: Centralize communication across channels

- Consolidate channels into one claim-linked thread

- Enable adjusters to message individual parties or create group messages for centralized communication

- Provide real-time updates so customers receive proactive visibility into claim status

Strategy 4: Standardize evaluation and settlement readiness

- Standardize how key facts are captured and summarized at each stage

- Use AI to reduce time spent sorting and reorganizing documentation

- Track what blocks settlement and optimize around those specific blockers

How is AI used in claims processing?

With those strategies in place, the next question is how AI is used in claims processing to deliver the greatest impact. AI and claims automation accelerate decision-making across each stage of the lifecycle by reducing manual work and ensuring adjusters have complete, organized information when they need it. The multi-cloud data engineering framework demonstrates this at an infrastructure level: a scalable, cost-efficient approach that leverages AI technologies has delivered an 88% improvement in claims processing speeds.

To build your own AI roadmap, prioritize the parts of the lifecycle with three characteristics: high volume, high repetition, and clear success criteria.

High volume: FNOL intake and customer communication

FNOL is the highest-leverage automation target because every claim passes through it. Assured improves FNOL automation by turning intake into a structured, guided workflow, both through digital self-service solutions and Sidekick, Assured’s call center solution. Using dynamic question flows, questions adapt based on what is already known (policy, loss details, property or vehicle, parties involved) and what is required for the specific claim path. You collect the right data, in the right order, with consistent structure every time.

Customer communication is equally high-volume. Status updates, document requests, clarification questions, service coordination, and follow-ups create constant back-and-forth. When this outreach is manual, cycle times stretch, adjusters spend their days on administrative exchanges instead of claim decisions.

Emma autonomously manages high-volume claim interactions across channels. Grounded in structured claim data, Emma understands what has already been collected, what is still needed, and what needs to happen next. It proactively initiates outreach, requests missing documentation, clarifies inconsistencies, and provides real-time status updates without waiting for adjuster prompts.

High repetition: Document collection and service scheduling

Document collection is an ideal target for agentic automation because it is repetitive, rules-based, and generates significant friction when handled manually. An AI agent can proactively request missing items and validate that submissions are complete and usable, keeping the file moving forward and freeing adjusters for higher-value work.

Vendor coordination is a hidden cycle time driver, especially for property claims. When scheduling is prompt, repair timelines stay on track, and satisfaction improves. Assured’s automatic service assignment routes eligible claims and enables self-scheduling with contractors, inspectors, and other service providers.

Clear criteria: Post-FNOL follow-ups that should not require phone calls

Many follow-ups are structured by nature: Send this document, confirm this detail, sign this form. When you digitize and automate these steps with an agentic AI assistant, the file keeps moving, even outside of business hours.

Claims automation in triage and routing

Triage is where cycle time is won or lost. Routing low-complexity claims into a fast path increases straight-through processing rates and protects adjuster capacity for complex files. When triage decisions are informed by complete, structured FNOL data, your routing accuracy improves and more claims qualify for automated handling.

This is especially important during CAT events, when claims can surge and adjusters need added support. Assured’s CAT solution proactively prepares policyholders for incoming CAT events, with extremely precise targeting. During CAT events, it helps adjusters effectively triage and route claims so that systems aren’t overwhelmed.

How to measure claims processing optimization

As you implement these strategies, you need a scorecard that ties operational changes to business outcomes. The right KPIs connect your claims automation investments to the metrics your leadership team tracks.

A practical measurement framework includes:

- Cycle time by claim type and channel

- Reopen and supplement rate with associated reason codes

- Number of outbound follow-ups per claim, by category

- Phone call volume per claim and the drivers of inbound status calls

- Adjuster capacity, measured as claims closed per adjuster and time spent on administrative tasks

- Customer experience indicators, including satisfaction rate, complaint rate, and digital adoption rate

When you implement structured intake plus automation, you should see improvement in the leading indicators first: fewer follow-ups and fewer calls. As the claim progresses, those improvements compound into faster cycle time, lower LAE, and a stronger customer experience.

The future of claims processing: AI, agentic automation, and scalable workflows

The strategies and AI applications outlined above represent what leading carriers are deploying today. The next phase of claims processing combines structured data, multiple types of AI architectures, and modular automation systems to support even greater accuracy, speed, and scalability. For claims leaders evaluating how AI is used in insurance claims, structured data remains the foundation. Advanced claims automation builds on that foundation to unlock new levels of performance.

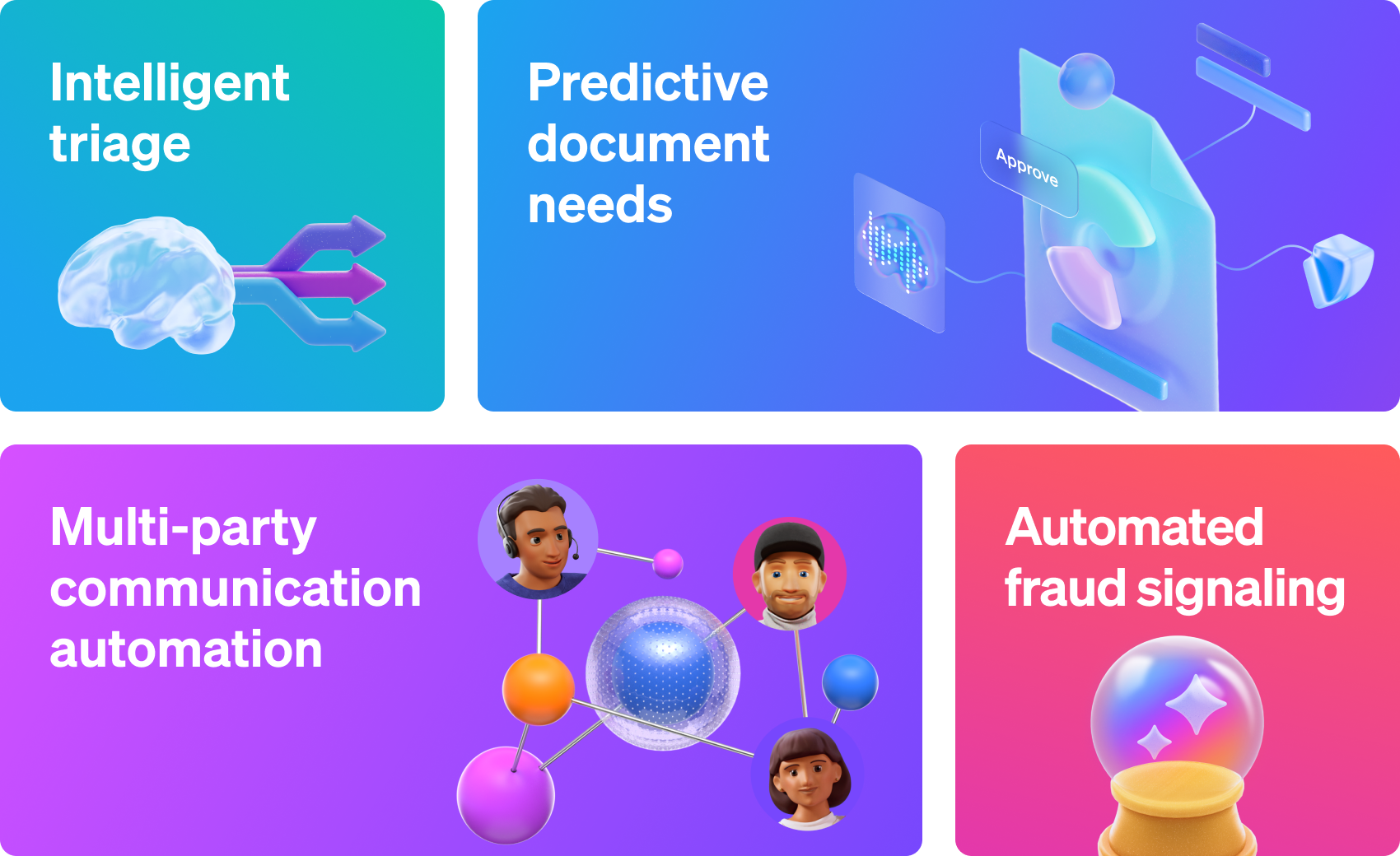

Several trends are defining what comes next:

- Intelligent triage: AI systems are beginning to assess severity, coverage complexity, jurisdictional nuances, and fraud indicators at intake. Claims are dynamically routed based on risk and effort, ensuring adjusters focus where human judgment adds the most value.

- Predictive document needs: Instead of waiting for gaps to surface, AI anticipates required documentation based on claim type, policy terms, and prior patterns. Missing information is proactively requested, reducing rework and accelerating resolution.

- Automated fraud signaling: When structured data is enriched and normalized, traditional AI models can flag inconsistencies across policy history, external data sources, and behavioral signals. Fraud detection shifts from reactive investigation to real-time signaling.

- Multi-party communication automation: Agentic systems coordinate all stakeholders in parallel. Outreach, reminders, clarifications, and updates occur automatically, with escalation only when needed.

All of this depends on structured, machine-readable data. With it, generative AI, traditional AI, and agentic systems operate with precision inside defined decision architectures.

The infrastructural shift is equally important. Modular, API-first platforms are replacing monolithic claims systems. You no longer need multi-year core overhauls to modernize. Instead, you layer automation around structured ingestion, integrate with existing systems, and deploy intelligence incrementally.

Better decisions start with better data

Throughout this guide, one principle has held at every stage of the claims processing lifecycle: the quality of your claims data at intake determines the speed and consistency of everything that follows. Whether you are focused on reducing cycle time, lowering LAE, or improving policyholder satisfaction, the path runs through structured, machine-readable data from first notice of loss.

Every carrier's insurance claims process has different pressure points. Your claims automation roadmap will reflect your lines of business, your technology environment, and your operational priorities. What remains consistent is the foundation. When your data is structured from the first interaction, every stage of claims processing becomes faster, more consistent, and more measurable.

Assured is built around this principle. Structured, machine-readable intake makes downstream automation possible. Agentic AI then uses that structured context to handle high-friction work across the lifecycle: Collecting missing information, responding to inbound questions, and keeping claims moving 24/7.

Get a demo to learn how Assured can improve your claims processing lifecycle.

Subscribe for updates

You might also like

What is claims management? A guide for insurance leaders

Learn how to improve cycle time, reduce LAE, enhance CX, and support automation across claims.

By The Assured Team

Subscribe for updates

By providing your email, you indicate you have read and understood our Privacy Policy.