Your adjusters are managing growing claim volumes while policyholders expect faster, more transparent resolutions than ever before. Straight-through processing (STP) offers a path forward, bringing claims from first notice of loss (FNOL) to settlement without manual touchpoints. The result: Faster cycle times, lower loss adjustment expenses (LAE), and dramatically better customer experiences.

Now, AI is transforming the automation landscape, making straight-through processing in insurance finally possible. McKinsey predicts that by 2030, more than half of current claims activities will be handled through automation.

As AI unlocks new possibilities for carriers, achieving STP requires a fundamental shift in how claims organizations think about AI-powered claims automation and the structured data foundation it depends on. Assured is leading this change, with AI-driven solutions that are already delivering straight-through processing at enterprise scale for the nation’s top carriers.

Assured: The leading AI platform in P&C

Trusted by the nation’s top insurers, Assured processes tens of millions of claims each year, delivering straight-through processing at enterprise scale.

Learn moreWhy STP matters for claims operations leaders

From a business perspective, straight-through processing in insurance is compelling across every metric. Speed improves. Costs drop. When claims move through the lifecycle with minimal manual intervention, carriers see immediate gains in both areas.

STP in insurance reduces cycle time by accelerating resolution through complete, consistent data from the start, while ensuring low-complexity claims no longer compete with complex losses for adjuster attention.

STP improves efficiency, accelerates settlement, reduces costs, and improves CX, all of which are key concerns for CCOs, VPs of Claims Ops, and Innovation leaders. It eliminates avoidable operational friction and reduces cycle time variance across adjusters.

Why do fewer insurers achieve STP?

Everyone in insurance is chasing straight-through processing, yet very few achieve it. The reason is not a lack of technology investment. The reason is data.

Achieving straight-through processing requires a foundation of quality data. Most claims data gathered at intake is often low-quality and unstructured. Open-ended questions yield open-ended answers. Multiple intake channels create fragmentation. Without quality data, there is no foundation for downstream automation.

Most claims workflows compound this problem. Adjusters spend hours chasing missing information, reconciling inconsistent inputs, and manually transferring data between systems. By the time a claim is ready for adjudication, the opportunities for automation have already passed. AI performs best when built on clean, structured inputs.

The data is just the start. Beyond just collecting quality data, building on top of it is still challenging and requires very sophisticated process automation software.

Bolt-in AI solutions don’t achieve this. Assured does, with a suite of AI-driven solutions that are designed to unlock downstream automation and straight-through processing for P&C carriers.

How structured data unlocks STP at scale

Solving the problem starts at the source. Straight-through claims processing requires structured, machine-readable data from the very first interaction. This means capturing standardized inputs at FNOL that downstream systems can act upon without human translation.

When data is structured from the start, AI models can interpret claim context, and automated workflows can route claims appropriately. The result is higher claim resolution rates and fewer manual touchpoints.

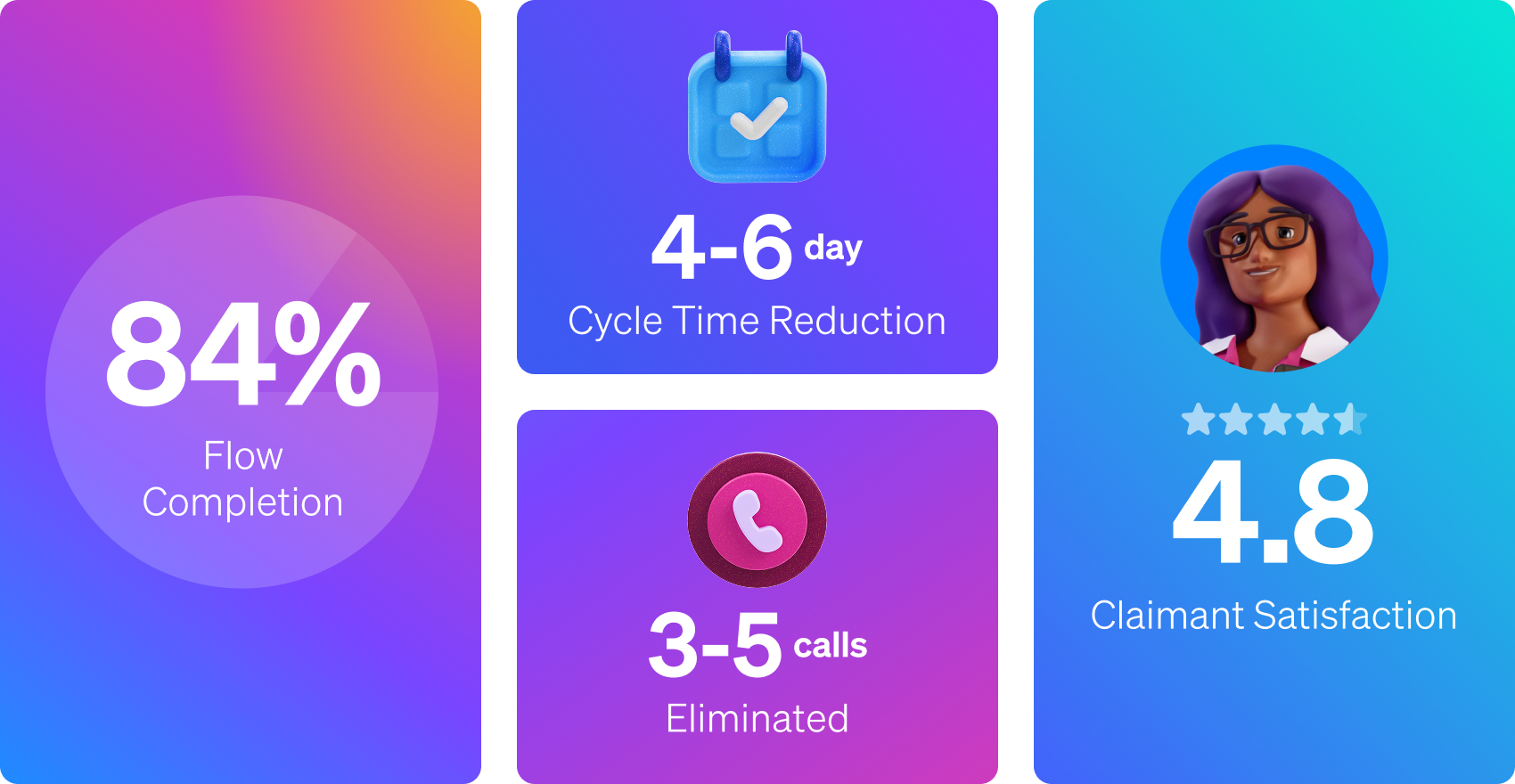

Assured's platform addresses this challenge head-on by gathering structured data on 100% of claims from the start. Carriers using Assured report 4-6 day reductions in cycle time, 84% flow completion rates, and 3-5 fewer phone calls per claim on average.

What straight-through processing means for claims

With the business case established, it helps to define exactly what STP entails. In insurance, straight-through processing means a claim can move from FNOL to final settlement without requiring manual intervention. The concept of STP originated in financial services during the 1990s to accelerate equities trading. Insurance adopted the framework later, applying it first to underwriting before extending to claims.

It’s important to clarify what straight-through processing is and what it is not. Straight-through processing is not a single feature, rule, or automation shortcut. It is an operating model. STP defines how claims flow from start to finish: Automation handles routine decisions, while adjusters step in for cases that require human judgment.

Straight-through claims processing aims to improve efficiency, reduce human error, and free up staff for higher-value work.

When STP is working, your adjusters focus on complex cases and customer-facing decisions, not missing information or correcting basic errors.

Today, straight-through claims processing is the operational gold standard. A gold standard Assured achieves by building a platform with structured data at the core. This makes touchless claims and STP a current reality.

How AI accelerates straight-through claims processing

Artificial intelligence is accelerating insurance claims processing in ways that were impossible just a few years ago. Generative AI can summarize documents and extract key data points. Agentic AI goes one step further, taking autonomous action to gather missing information, respond to user questions, and move claims forward without adjuster intervention.

But AI is only as good as the data it receives. Models trained on unstructured, inconsistent inputs produce unreliable outputs. Models powered by clean, structured data deliver true automation. Assured’s approach, built around structured data from intake, delivers straight-through processing for insurance claims at enterprise scale.

How STP works across the claims lifecycle

Understanding the value of STP is one thing. Seeing how it works in practice is another. Straight-through processing is the outcome of systems built on structured data and AI-powered automation. When those elements are in place, claims can move from first notice to resolution with minimal human intervention. STP depends on data quality from the first interaction.

In claims processing, each automation step depends on the quality and consistency of the data captured upfront. Clean, structured inputs allow automation to scale at every stage of the claims lifecycle.

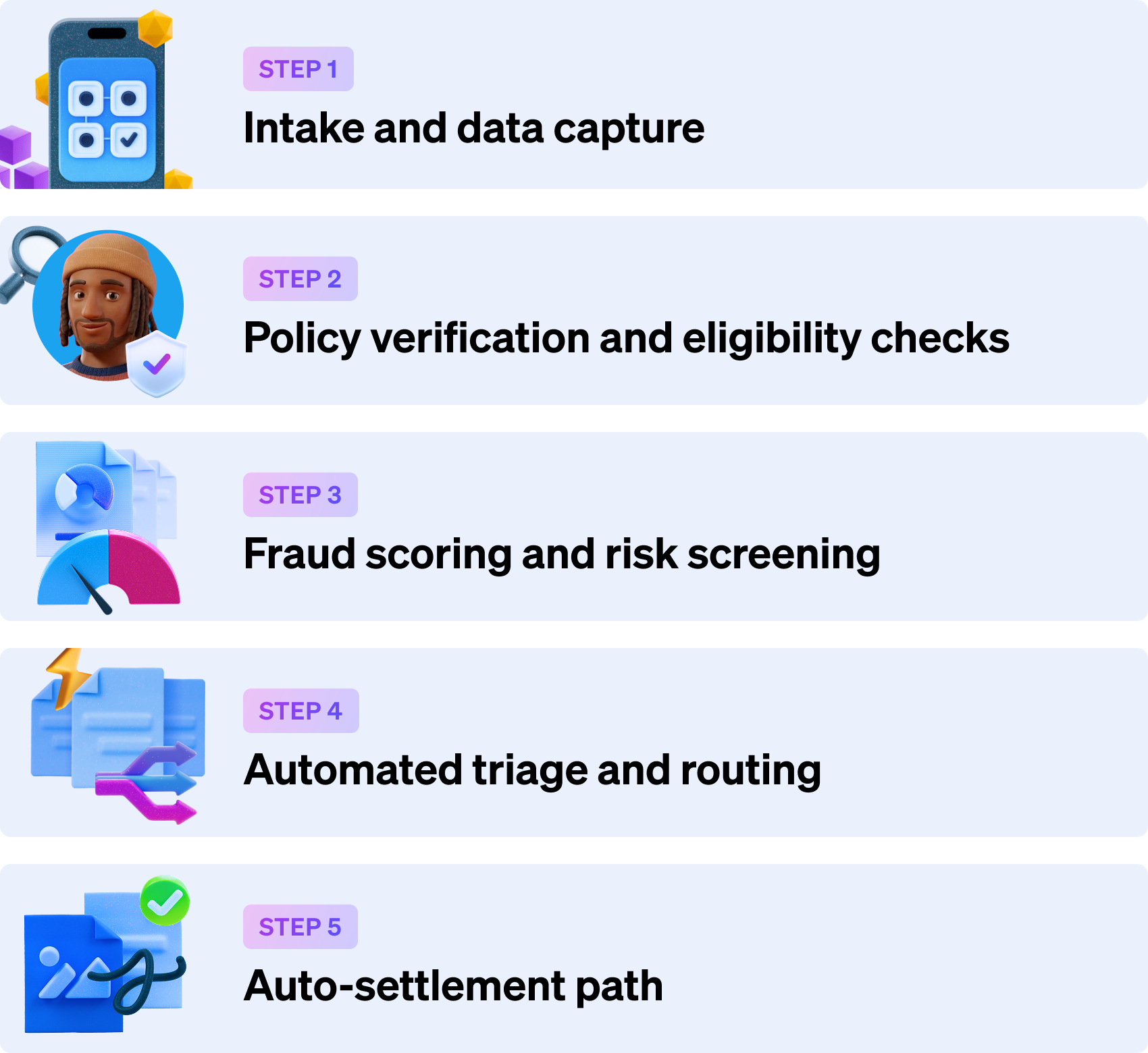

Step 1: Intake and data capture

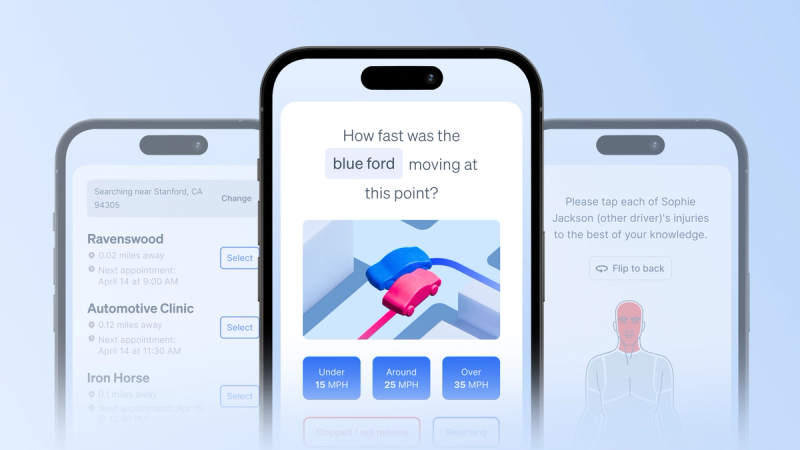

Structured FNOL data determines whether a claim qualifies for straight-through processing. If key details are missing? STP stops before it starts. Assured’s digital claims intake workflow adapts questions in real time, capturing complete, machine-readable data for every claim. In addition to self-service solutions, Sidekick supports call centers by ensuring every adjuster asks the right questions to collect quality data at FNOL.

Step 2: Policy verification and eligibility checks

The system validates coverage, limits, deductibles, and exclusions against policy data automatically. All involved parties are automatically contacted to collect additional information. When information is incomplete, an agentic AI assistant immediately prompts claimants to fill the gap, before it becomes the adjuster’s problem. All conversations across channels are consolidated in one place with omnichannel communication and centralized messaging. The result: claims keep moving without human review.

Step 3: Fraud scoring and risk screening

While other processes run, an automated fraud solution evaluates risk signals on each claim in parallel. Low-risk claims continue uninterrupted. Claims with anomalies or elevated risk are flagged and routed for human review before costs escalate.

Step 4: Automated triage and routing

Eligible, low-complexity claims move directly into automated paths. Complex, ambiguous, or multi-exposure claims take a different route: straight to the right adjuster with full context rather than a blank file.

Step 5: Auto-settlement path

Low-severity claims such as glass-only auto, minor collisions, or basic property losses can settle without adjuster handling. Automated digital service assignment lets adjusters seamlessly schedule tows, rentals, and other necessary services for claimants. Payments, communications, and documentation are completed automatically.

Which insurance claims qualify for straight-through processing

In insurance, straight-through processing works best when claims are predictable and low risk. Not every claim qualifies, but that is the point. STP is designed to accelerate the right claims while preserving human judgment where it matters most.

Historically, straight-through processing was limited to the simplest claims. Glass-only auto losses, minor single-vehicle collisions with clear fault, small property claims involving limited water or wind damage, and single-party events without injuries were the strongest STP candidates. High STP rates are also strongly associated with P&C lines when products are sold directly.

Claims involving potential fraud indicators, unclear liability, multiple vehicles or parties, bodily injury, or disputed facts typically fell out of STP eligibility. These files required additional documentation, manual clarification, and repeated follow-ups, increasing adjuster workload and driving up LAE.

Assured makes it possible for carriers to achieve high STP rates, even in high-complexity cases. Regardless of complexity, carriers using Assured regularly achieve up to 80% STP rates for auto claims. This is where agentic AI assistants like Emma play a critical role. When a claim is close to qualifying for STP but lacks key information, Emma proactively gathers missing details and clarifies inconsistencies with involved parties, handling nearly 70% of interactions autonomously.

By closing data gaps early, Emma increases the number of claims eligible for straight-through processing.

The result is meaningful automation across higher-complexity files that traditionally consumed the most adjuster time.

How STP benefits claims operations

When all these elements work together, the operational impact shows up directly in LAE. In insurance, straight-through processing reduces friction and lowers costs while allowing claims teams to scale without adding headcount. It reduces manual touches, eliminates redundant follow-ups, and compresses cycle time. This translates directly into lower LAE across all lines of business.

Customer experience improves alongside efficiency. Faster resolutions, proactive updates, and clearer next steps increase transparency, which translates to higher Net Promoter Scores. When policyholders don’t need to repeat information or wait days for basic updates, trust increases.

STP also strengthens scalability during catastrophic events. When volume spikes, CAT solutions absorb demand without overwhelming adjusters. Claims that qualify continue to flow, while complex cases are triaged appropriately.

How to increase your straight-through processing rates

Achieving STP depends on a few key elements. Here are some strategies to improve STP rates right away.

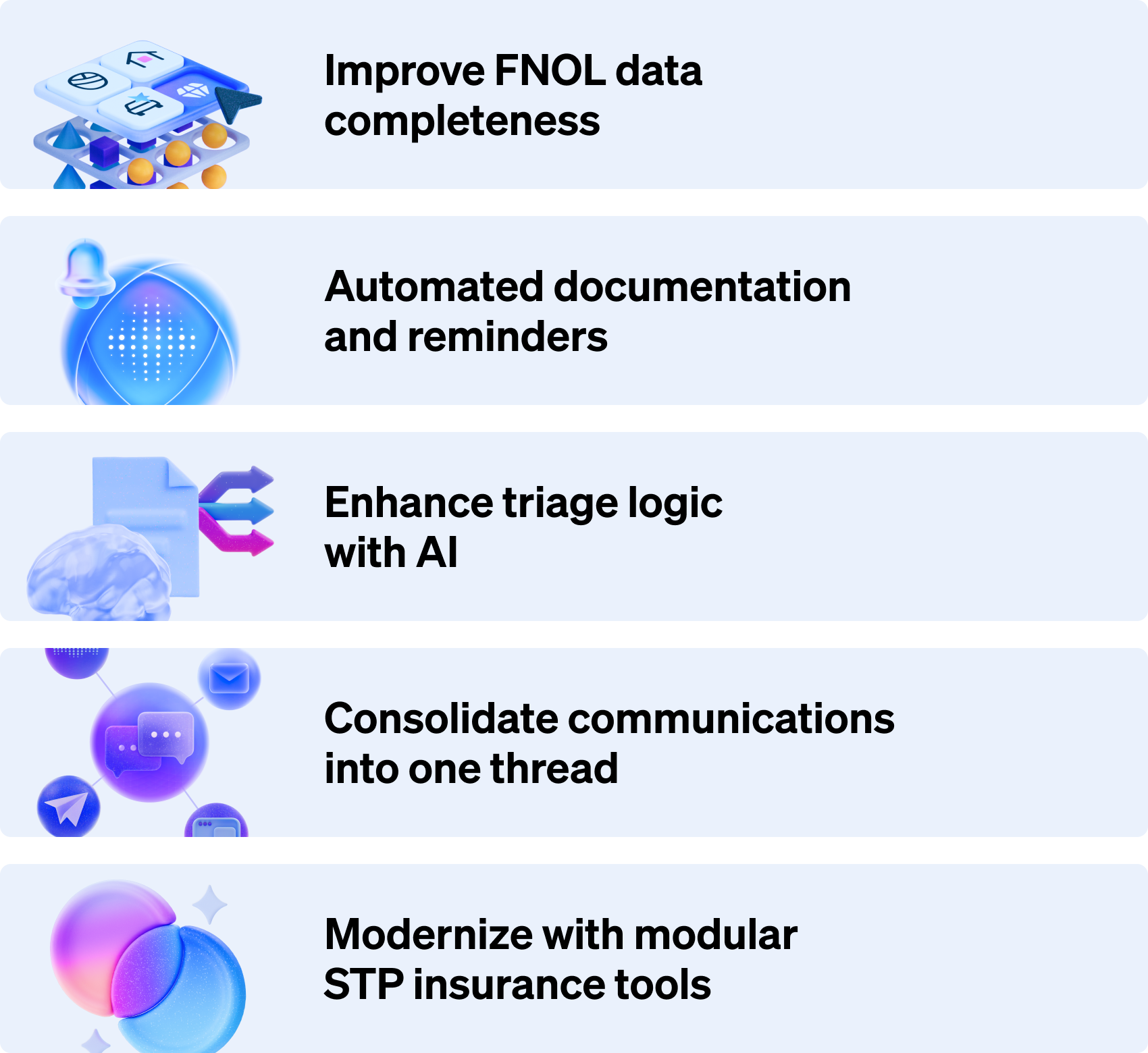

Strategy 1: Improve FNOL data completeness

Structured FNOL data directly increases STP eligibility. When intake captures the right details up front, claims move forward without delays.

Strategy 2: Use automated documentation and reminders

Why wait for adjusters to chase documents manually? Automated requests and reminders validate data up front and reduce idle time. Claims move toward settlement readiness faster.

Strategy 3: Enhance triage logic with AI

AI-driven triage logic evaluates severity, exposure, and risk early in the process. The result is improved routing accuracy, fewer reassignments, and claims entering the correct path the first time.

Strategy 4: Consolidate communications into one thread

Fragmented communication across email, SMS, and phone calls makes it harder to maintain complete context. A unified claims messaging platform consolidates everything in one place, enabling downstream automation to function reliably.

Strategy 5: Modernize with modular STP insurance tools

Modern STP insurance platforms are modular by design. These platforms integrate with existing core systems, allowing carriers to improve STP incrementally without replacing their entire stack.

What leading carriers do differently to achieve STP

If you're achieving high STP rates, you likely share these characteristics with other leading carriers. They prioritize data quality at intake over downstream remediation and deploy modular solutions that integrate with existing core systems. They measure STP rates rigorously and iterate continuously based on what the data reveals.

Today, technology exists to enable full STP insurance capabilities for simple claims with predictable characteristics. Carriers that start with clean, structured data from FNOL are the ones achieving what the industry has long envisioned. The path forward starts with a single decision: Prioritize structured data from the first interaction.

Straight-through processing insurance is an operational imperative, and one that Assured is already helping carriers achieve today. Carriers that have true STP insurance capabilities outperform on every metric that matters: Speed, cost, accuracy, and customer experience. Better decisions start with better data. And better data starts at the very first interaction.

See how leading P&C carriers achieve 40-50% cycle time reduction with Assured's structured data platform.

Schedule a 30-minute demo to learn more.

Last modified on May 28, 2026

Subscribe for updates

You might also like

FNOL automation: How AI is transforming claims intake

Learn how AI-powered FNOL automation helps carriers reduce cycle time and improve accuracy.

By The Assured Team

Subscribe for updates

By providing your email, you indicate you have read and understood our Privacy Policy.